323 / 762

323 / 762

Chapter 8: Discrete Probability Distributions

323

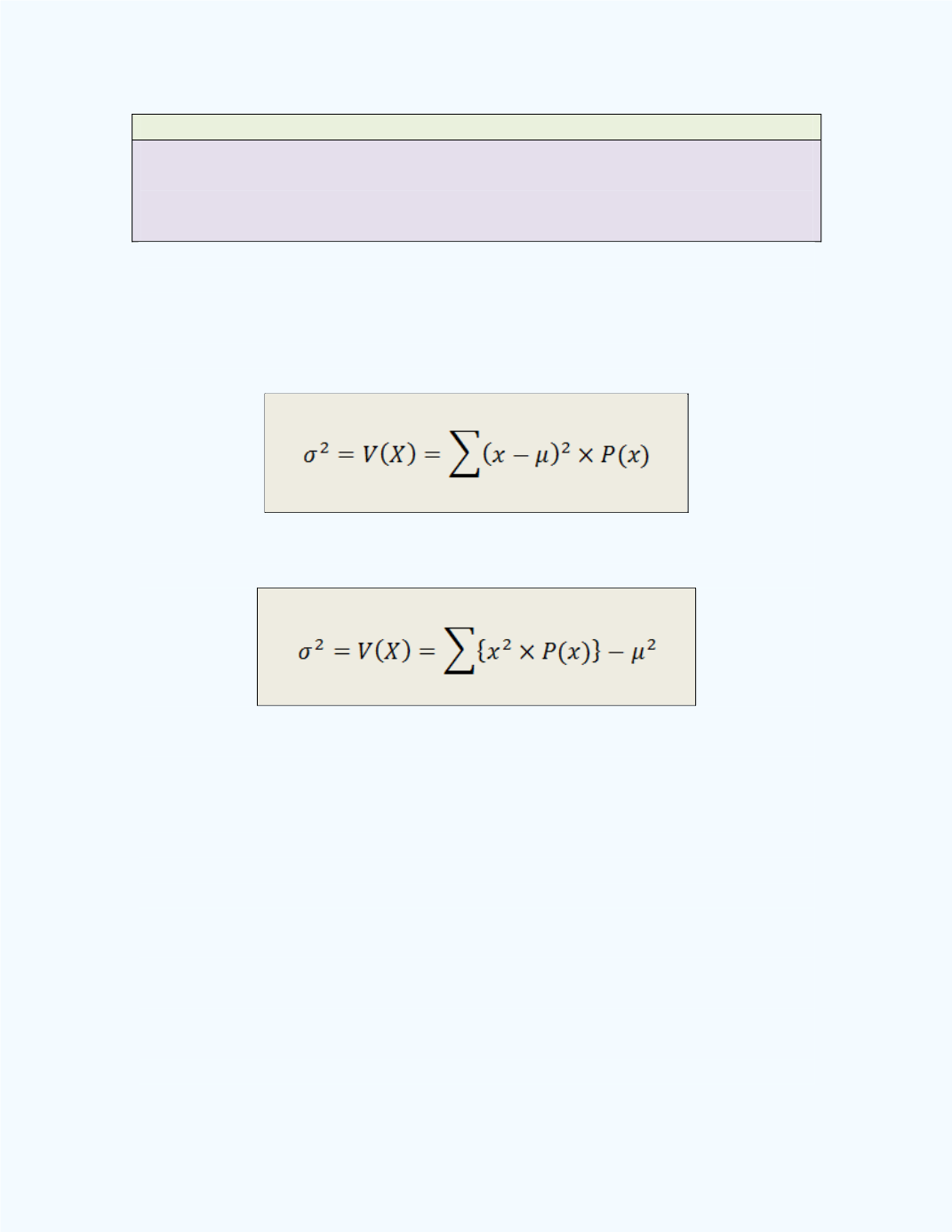

Definition: Variance for a Discrete Random Variable

The variance for a discrete random variable

X

measures the spread of the

random variable about the expected value (mean

).

The variance is usually denoted by

(read as “sigma square”) or V(

X

) and

is obtained by computing the expected value of the squared deviations from

the mean

. The formula is given next. The weights here will be the values

of the probabilities associated with the values of the random variable.

An equivalent computational formula for the variance is given as

In both equations,

is the expected value for the random variable

X

.

Also, in the above formula, the summation is only for

} over

all the

x

values. The variance for a probability distribution is equal to its

population variance.

Example 8-6:

What is the variance of the winnings for a raffle with a first

prize of $1000, a second prize of $500, and a third prize of $300 if 1,000

tickets are sold?

Solution:

Let the winnings for the raffle be represented by the random

variable

X

. First we need to compute the mean,

for

X

. In order for us to

complete the computation for

we will have to derive the probability

distribution for

X

. If we assume that the tickets are drawn at random without

replacement, then the probability of winning the first prize will be 1/1000;